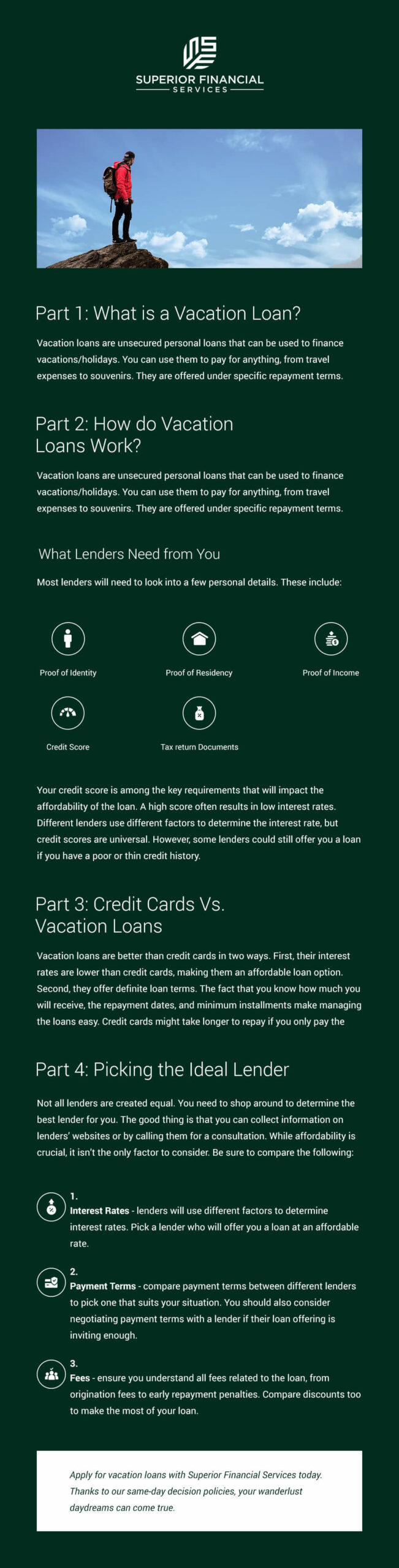

Nothing comes closer to the feeling of spending quality time with friends and family. Vacations provide just that. You get to hang out with your loved ones away from the distractions of normal life, from busy work schedules, and necessary commitments. However, this doesn’t make going on a vacation cheap.

You will have to pay for travel expenses, cozy accommodation, finger-licking cuisine, and sentimental souvenirs. What if you don’t have enough cash to finance your dream vacation? Vacation loans can help turn your dream getaway into a reality. While COVID-19 complicated travel for many, many travel-lovers have been using the time to dream up their dream vacations or find unique ways to travel despite limitations. Understanding how these loans work could help finance your holiday now, next year, or whenever you’re ready to hit the road!

Here is an overview of vacation loans and how they work.

What is a Vacation Loan?

A vacation loan is simply a branded personal loan. Lenders offer it to customers to fund travel expenses. You will be given a specific amount of cash under specific repayment terms. Ideally, the repayment terms depend on the lender’s specific criteria and your credit score. Since most loans are unsecured, you don’t have to put up collateral to qualify.

Some vacation loan lenders are lenient enough to offer loans to people with poor credit scores. You can use the loan to finance all types of vacation expenses, from travel expenses to accommodations, food, and souvenirs.

How Vacation Loans Work

Just like most unsecured loans, these loans are based on installments. You get to pay a specific amount over a period of time—many lenders offer short-term loans that can be repaid within a year. However, the loan terms and interest rates tend to vary from one lender to another.

During the application, you provide your personal details, including employment history, salary, and current job title. Perhaps the most important part of the application process is your credit score. A high score will increase your chances of getting a vacation loan at an affordable interest rate. If you have a subpar credit score, leverage common best practices to improve it, and turn to a lender who will work with you even if your credit score is below average.

Why Vacation Loans are Better Than Credit Cards

When it comes to financing vacations, credit cards have a few benefits, especially if yours allows you to accrue travel reward points. These points could help lower travel expenses and save you money. If all other factors held constant, it would be wiser to finance your trip with a vacation loan.

One huge differentiating factor between the two is that credit cards tend to have a higher interest rate, which makes them less affordable. Unlike credit cards, you will know the exact total amount and maturity date of your loan when you choose loans. This makes planning your trip and identifying whether borrowing is worth it.

How to Compare Lenders